The amount of time, money and effort spent obtaining Portugal residency depend on each applicant’s circumstances.

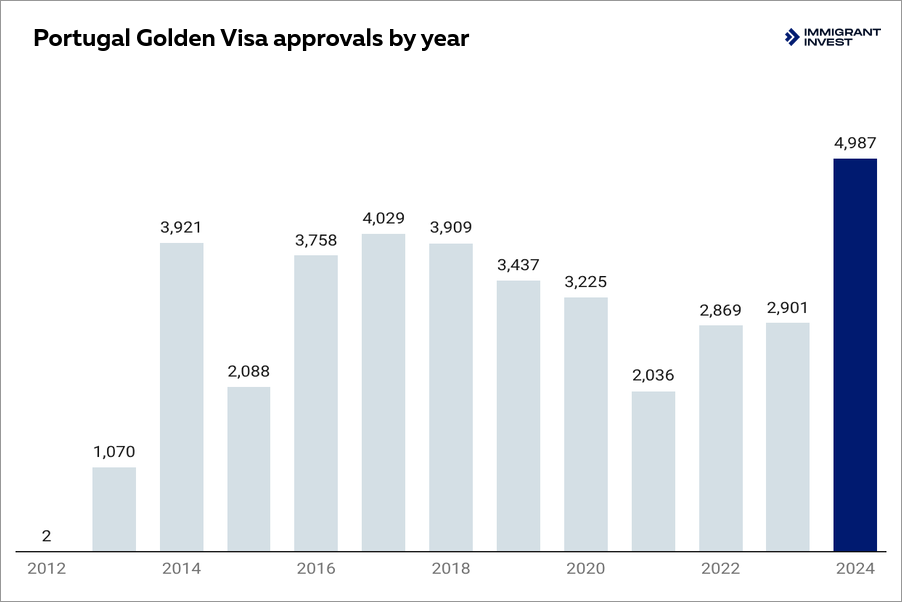

For instance, those willing to get a Golden Visa must invest at least €250,000. They will obtain their residency cards in 12+ months.

On the other hand, the obtaining period for a Global Talent Visa is 4 months. However, applicants must first establish cooperation with a recognised Portuguese university or research institution and prove that their professional background is relevant to the selected project.

Processing time of applications for long-term visas for family reunification, study, or scientific research, strongly depends on the completeness of the candidate’s list of documents.

Hello, I want to buy an apartment in Portugal to come there for vacations with my family. Can I get residency based on this?

Hello,

Thank you for your question.

Purchasing property in Portugal does not grant eligibility for residency. This was previously possible through the Portugal Golden Visa programme, but the real estate option was suspended in 2023.

To obtain residency, you may consider alternative routes. For example, if you intend to relocate to Portugal and have passive income from abroad, you may apply for the Visa for Financially Independent Persons.

If your aim is to visit Portugal occasionally, the Portugal Golden Visa may still be suitable, as it requires only a minimum stay of seven days per year. It is currently available for investments starting from €250,000.

To determine the best option for your situation, sign up for a one-to-one meeting with Immigrant Invest.

Hello,

I have a question about a digital nomad visa. You say that there are two types. If I obtain a one-year visa, can I then turn it into a permit?

Hello,

Thank you for your question.

No, a one-year temporary stay visa for Portugal cannot be converted into a residence permit. After the visa expires, the digital nomad must leave the country.

To obtain Portuguese residency as a digital nomad, you will need to apply for a residency visa. This visa is valid for 4 months and allows entry into Portugal to apply for residency.

Hello I wondered if I can work in France if I obtain a passive income visa to Portugal?

Hello Anika,

Thank you for your question.

None of the residence permits obtained in Portugal allow you to work in another EU state. To work in France, you will need to obtain a corresponding residence permit there.

However, with a Portugal D7 visa, you can travel visa-free across the Schengen Area and stay for up to 90 days within a 180-day period.